Popping the Gross-to-Net Bubble, Part III: The Pharmacy Benefit

How pharma manufacturers can steadily navigate GTN components and complexities when planning pharmacy benefit reimbursement.

Welcome to the third installment of my “Popping the Gross-to-Net Bubble” series. In my previous column, I explored actionable steps pharmaceutical manufacturers can take to address gross-to-net (GTN) challenges for products reimbursed under the medical benefit. This time, I focus on products reimbursed under the pharmacy benefit.

The complexity of gross-to-net in the pharmacy benefit

Managing GTN for the pharmacy benefit is significantly more complex than for the medical benefit, due to its wide variability across payer types and product archetypes.

Payer types include commercial, Medicare, Medicaid, health maintenance organizations (HMOs), 340B, and government accounts, such as the VA, DoD, and Indian Health Service, while product archetypes feature general medicine brands, generics, vaccines, specialty lite, specialty, specialty generics, biosimilars, and orphan/rare products.

Why net revenues suffer

From our 24 years of experience working with pharmaceutical companies, we’ve seen many new product planning, pricing, and market access teams prioritize large commercial pharmacy benefit managers (PBMs) first, as they cover the most lives. However, the focus is typically on achieving formulary coverage rather than optimizing net revenue—a key driver of poor GTN performance.

Instead, we recommend starting with statutory discounts such as Medicaid unit rebate amount (URA), 340B, and Federal Supply Schedule (FSS), as they are fixed costs that can significantly impact GTN if not properly managed in relation to commercial payer decisions.

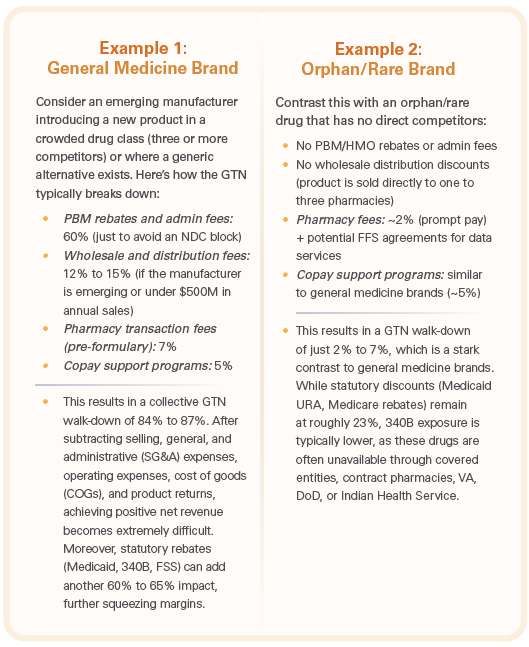

GTN in different product archetypes

Let’s examine how GTN varies between two contrasting product types: general medicine brands and orphan/rare brands.

The two examples at right (click to enlarge) represent the GTN spectrum. Other product types such as specialty and specialty lite drugs fall somewhere in between, depending on factors such as budget impact analysis, payer contracting, clinical profile, and access restrictions (e.g., step edits, prior authorization, catastrophic coverage, etc.).

Key components of GTN and manufacturer strategies

Pharma manufacturers must navigate six key GTN components when planning for pharmacy benefit reimbursement:

1. Statutory discounts

Manufacturers should start with statutory discount analysis based on channel and payer mix. Products sold to government accounts (Medicaid, Medicare, VA, DoD, Indian Health Service, etc.) are subject to mandatory rebates, which must be accounted for upfront.

2. Payer discounts (PBMs & HMOs)

After assessing statutory discounts, manufacturers determine PBM and HMO rebates and admin fees. These discounts directly impact formulary positioning, patient access, and out-of-pocket costs. However, the net pricing decisions here will also influence statutory discount liabilities, making this a critical risk area.

3. Site of care & GPO discounts

Manufacturers must consider whether discounts should be extended to sites of care (e.g., hospitals, infusioncenters) either directly or via GPO contracts. Pre-formulary coverage discounts may help drive early adoption. Additional discounts for outpatient pharmacies typically apply only to long-term care facilities or hospital-affiliated GPO networks.

4. Distribution discounts

Prompt pay discounts vary by distributor type. Additional fees beyond bona fide FFS depend on manufacturer size, portfolio breadth, and time on market. Many emerging manufacturers are now bypassing wholesalers and selling directly to sites of care to reduce excessive distribution costs.

5. Patient affordability programs

Traditionally designed and directed by marketing or brand teams, patient support programs are often finalized after PBM negotiations. Manufacturers have historically aimed for $0 to $35 copays for commercially insured patients, but this strategy needs reevaluation as Medicaid copays cannot be bought down; Medicare OOP costs are now capped at $2,000 annually (effective 2025); copay accumulator and maximizer programs limit the effectiveness of affordability programs; and manufacturers are becoming more strategic about applying affordability support to avoid wasted resources.

6. Penalty discounts & price increase strategy

Price increases must be carefully planned due to rebate penalties from Medicaid and Medicare. Outpacing the consumer price index results in perpetual penalties, impacting 55% of the pharmacy benefit market represented by Medicaid and Medicare collectively. The removal of the average manufacuter’s price (AMP) cap (effective Jan. 1, 2024, under the American Rescue Plan Act of 2021) has led some manufacturers to exit Medicaid due to negative GTN scenarios. Manufacturers must align pricing strategy with GTN management to avoid unintended financial consequences.

The key to managing GTN: Strong cross-functional governance

Pharma companies that effectively manage GTN integrate finance and government pricing teams into decision-making alongside marketing, field sales, market access, trade and distribution, and patient services. Conversely, companies that struggle with GTN allow each of these groups to operate independently, with finance and government pricing teams relegated to support roles rather than strategic partners.

As pricing pressures increase under the IRA and Medicaid AMP cap removal, we anticipate finance and government pricing teams will play an even greater role at the executive level.

Looking ahead

In my next installment, I’ll examine examples of how pharmaceutical manufacturers have successfully and unsuccessfully navigated GTN challenges. I’ll highlight common pitfalls and lessons learned that can help manufacturers avoid costly mistakes.

About the Author

Bill Roth is General Manager and Managing Partner of IntegriChain’s consulting business, which includes Blue Fin Group, a strategy consulting company he started in 2001, and the IntegriChain advisory services business.